Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return Page 16

Download a blank fillable Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form 706 - United States Estate (And Generation-Skipping Transfer) Tax Return with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

Tax Return Printable pdf") 1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12 13

13 14

14 15

15 16

16 17

17 18

18 19

19 20

20 21

21 22

22 23

23 24

24 25

25 26

26 27

27 28

28 29

29 30

30 31

31Form 706 (Rev. 8-2012)

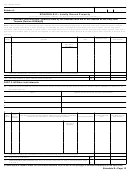

Decedent’s social security number

Estate of:

SCHEDULE I—Annuities

Note. Generally, no exclusion is allowed for the estates of decedents dying after December 31, 1984 (see instructions).

Note. If the value of the gross estate, together with the amount of adjusted taxable gifts, is less than the basic exclusion amount and the

Form 706 is being filed solely to elect portability of the DSUE amount, consideration should be given as to whether you are required to

report the value of assets eligible for the marital or charitable deduction on this schedule. See the instructions and Reg. section 20.2010-2T

(a)(7)(ii) for more information. If you are not required to report the value of an asset, identify the property but make no entries in the last three

columns.

Yes No

A

Are you excluding from the decedent’s gross estate the value of a lump-sum distribution described in section

2039(f)(2) (as in effect before its repeal by the Deficit Reduction Act of 1984)? .

.

.

.

.

.

.

.

.

.

.

.

.

If “Yes,” you must attach the information required by the instructions.

Item

Description.

Alternate valuation

Includible alternate

Includible value at

number

Show the entire value of the annuity before any exclusions

date

value

date of death

1

Total from continuation schedules (or additional statements) attached to this schedule .

.

TOTAL. (Also enter on Part 5—Recapitulation, page 3, at item 9.) .

.

.

.

.

.

.

.

.

(If more space is needed, attach the continuation schedule from the end of this package or additional statements of the same size.)

Schedule I—Page 16

ADVERTISEMENT

0 votes

Related Articles

Related forms

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return")

Tax Return - 2011") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2011

Financial

Tax Return - 2008") Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Instructions For Form 706 - United States Estate (and Generation-skipping Transfer) Tax Return - 2008

Financial

Tax Return - 2005")

Tax Return")

Related Categories

Parent category: Business