Form It-565 - Partnership Return Of Income Page 11

Download a blank fillable Form It-565 - Partnership Return Of Income in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form It-565 - Partnership Return Of Income with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

12Apportionment of Income Schedule

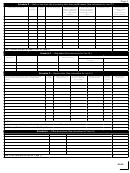

Section C. Computation of apportionment percent

Instructions

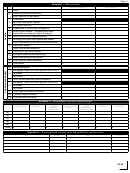

The Louisiana Income Tax Law creates a presumption that the apportion-

is completed shall be considered as the place at which the goods are

ment method of reporting must be used in the determination of the net

received by the purchaser. The Louisiana factor shall also include all

income where such net income is apportionable. It is mandatory that the

charges for services performed in Louisiana.

2. The Salaries and Wages Factor. The Louisiana wage factor shall

apportionment method be used unless it can be clearly shown that the

use of the apportionment method produces a manifestly unfair result,

include the total salaries, wages, and other personal service compen-

and permission to use the separate accounting method is granted by

sation paid during the taxable year for services rendered in Louisiana

the Secretary. The proportion of such income to be attributed to sources

in connection with the production of apportionable net income.

within this State should be determined by means of an apportionment

3. The Property Factor. The Louisiana factor shall be the average of the

percent based on the factors set forth below. The percent computed in

value of the taxpayer’s real property and tangible personal property

that schedule is the arithmetic average of the factors applicable to your

used in the production of apportionable income within this State:

operations, which factors depend on your principal kind of business.

a. at the beginning of the taxable year, and

b. at the end of the taxable year.

The “Louisiana Factors” are as follows:

4. The Loan Factor. In the case of a loan business, the Louisiana factor

1. The Sales and Charges for Services Factor. The Louisiana sales

shall be the amount of loans made in this State during the period for

factor shall include all sales made in the regular course of business

which the return is filed.

where the goods, merchandise, or property is received in this State by

For further information relative to these apportionment factors, see R.S.

the purchaser. In the case of delivery by common carrier or by other

47:245.

means of transportation, including transportation by the purchaser, the

place where the goods are ultimately received after all transportation

Section D. Apportionment factors to be used in determining income derived from sources partly within Louisiana

Not all of the following factors should be used. Your principal kind of busi-

which the use of property is not a material income-producing factor, use

ness determines which factors apply. For air transportation, use factors

factors (1) and (2), otherwise, use factors (1), (2), and (3); for loan busi-

(1) and (3); for pipeline transportation, use factors (1), (2), and (3); for

nesses, use factors (2) and (4); and, for merchandising, manufacturing,

other transportation, use factors (1) and (3); for service enterprises in

and other business, use factors (1), (2), and (3).

3. Percent (Col 2 ÷Col 1)

Description of items used as factors

1. Total amount

2. Louisiana amount

1.

Net sales of merchandise and/or charges for services

(a)

Sales where goods, merchandise, or property is received in Louisi-

00

00

ana by the purchaser..........................................................................

00

00

(b)

Charges for services performed in Louisiana ....................................

00

00

(c)

Other gross apportionable income .....................................................

Total (In Column 1, enter total net sales and charges for services; in

00

00

%

Column 2, enter total of Lines a, b, and c. Enter ratio in Column 3.) .........

2.

Wages, salaries, and other personal service compensation paid during

00

00

%

the year (Enter amounts in Columns 1 and 2, and ratio in Column 3.)

..

00

00

%

3.

Income tax proper ty factor ratio ..............................................................

4.

Loans made during the year (Enter amounts in Columns 1 and 2, and

00

00

%

ratio in Column 3.) .....................................................................................

%

5.

Total percents in Column 3 ........................................................................................................................................

6.

Average of percents (Divide Line 5 by number of factors used. Use result in determining income apportioned

to Louisiana on Page 1, Section A, Line 6.) ......................................................

%

................................................................

Explanation of Louisiana business

1.

Describe the nature of your business activity and specify your principle product or service, both in Louisiana and elsewhere.

Louisiana _________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

Elsewhere ________________________________________________________________________________________________

________________________________________________________________________________________________________

2. Give address and descriptions of places of business within Louisiana __________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial