Form It-565 - Partnership Return Of Income Page 10

Download a blank fillable Form It-565 - Partnership Return Of Income in PDF format just by clicking the "DOWNLOAD PDF" button.

Open the file in any PDF-viewing software. Adobe Reader or any alternative for Windows or MacOS are required to access and complete fillable content.

Complete Form It-565 - Partnership Return Of Income with your personal data - all interactive fields are highlighted in places where you should type, access drop-down lists or select multiple-choice options.

Some fillable PDF-files have the option of saving the completed form that contains your own data for later use or sending it out straight away.

ADVERTISEMENT

1

1 2

2 3

3 4

4 5

5 6

6 7

7 8

8 9

9 10

10 11

11 12

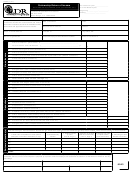

12State of Louisiana

IT-565B (1/12)

Department of Revenue

Apportionment

of Income Schedule

Please do not write in this space.

Name of partnership

Period covered by this return ____________________

Address

Requirements for filing – This form is to be attached to and filed with

City, State, ZIP

the Partnership Return (Form IT-565) if any partner who shares in the

profits or income of the partnership is not a resident of Louisiana and

a portion of the income is from business or property located outside

Louisiana. (See General Instructions below.)

General Instructions

Under the provisions of the Louisiana Income Tax Law, nonresident individuals

of the first class of items can be determined by direct allocation and entered

are taxed on only the portion of their net income that is derived from property

as Items 7(a), (b), and (c) in Section A of this form. But, in the case of net

located, business transacted, or services rendered in Louisiana. Therefore,

income from business partly within and partly without the State, a percent of

in the case of a partnership having nonresident partners and having income

the net income must be apportioned to Louisiana (Item 6 in Section A), on

from sources both within and without the State of Louisiana, it is necessary

the basis of an apportionment percent computed in Section D. However, if

that the net income from business, property, or services in Louisiana of the

the Louisiana portion is entirely separable from the remainder, and the use

partnership be computed so that nonresident individuals participating therein

of the apportionment method would produce a manifestly unfair result, a

may report the proper amount on his individual return (Form IT-540B).

separate accounting may be made for Louisiana business and the total net

income therefrom entered as Item 8 in lieu of the apportionment described

in the previous sentence, if permission to use that method is secured from

In order to determine the amount of income earned in Louisiana, it is nec-

essary to separate all items of income into two general classes, namely;

the Secretary. For more precise information concerning the methods of al-

(1) those items that can be allocated directly to the State in which they are

location and apportionment, see Louisiana Revised Statutes 47:241 through

earned, such as Items 4(a), (b), and (c) in Section A and (2) those items of

47:245.

income that arise from business partly without the State. Louisiana’s share

Section A. Computation of Louisiana net income

00

1. Total net income of partnership ...................................................................................................................

00

2. Add any Federal income taxes deducted in arriving at net income shown above. ......................................

00

3. Net income from all sources ........................................................................................................................

4. Less: Allocable income from all sources (Attach schedule supporting each amount entered on

Lines a, b, and c below and Lines 7a, b, and c.)

00

(a)

Net rents and royalties ...................................................................................

(b)

Net profit from sales or exchanges of property (including such items as

stocks, bonds, land, machinery, and mineral rights) not made in the regular

00

course of business .........................................................................................

(c)

Other net allocable income ............................................................................

00

5. Balance-net income subject to apportionment ............................................................................................

00

6. Net income apportioned to Louisiana (Multiply Line 5 by percent from Line 6, Section D.) ........................

00

7. Add allocable income from Louisiana sources

(a) Net rents and royalties .......................................................................................

00

(b) Net profit from sales or exchanged property (including such items as stocks,

bonds, machinery, and mineral rights) not made in the regular course of

00

business. ..........................................................................................................

00

(c) Other net allocable income ................................................................................

00

8. Total net income from Louisiana sources ....................................................................................................

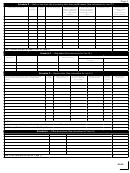

Section B. Distributive shares of nonresident partners

Enter in this schedule the name of each nonresident member and his distributive share in the portion of the net income of the partnership allocated to the

State of Louisiana (Item 8). Each partner's distributive share is deemed to apply ratably to taxable and nontaxable income, and to income from sources

within, as well as from sources without the State.

Social Security Number, name, and address of each nonresident partner as shown on his return.

Percentage

Social Security Number

of beneficial

Distributive share of net income to

or

interest

nonresident partner

Federal Employer ID Number

Name and address

(a)

%

00

(b)

%

00

(c)

%

00

(d)

%

00

(e)

%

00

2001

(f)

%

00

Totals

100%

00

ADVERTISEMENT

0 votes

Related Articles

Related forms

Related Categories

Parent category: Financial